Intro: Investors utilize different fund companies and managers in an attempt to diversify their holdings. But many fund companies, whether focused on mid-cap growth or large-cap value, may own the same names. Investors should review the top ten holdings of all funds in their portfolio.

Investments often come in different shapes and packages, but many have similar contents. For example, you may own two different mutual funds in your 401k that hold many of the same names.

That’s all well and good while the market sets new all-time highs day after day, but you may be setting yourself up for a fall. Bull markets take the stairs…bear markets take the elevator shaft.

Sometimes, all ships rise and fall with the tide. In instances where the markets get spooked and everyone runs for the exits, that’s when you learn why overlap is important. When investors capitulate to the stress of the volatility and watch their net worth evaporate away to nothing, they tend to want to sell out and go to all cash and wait it out.

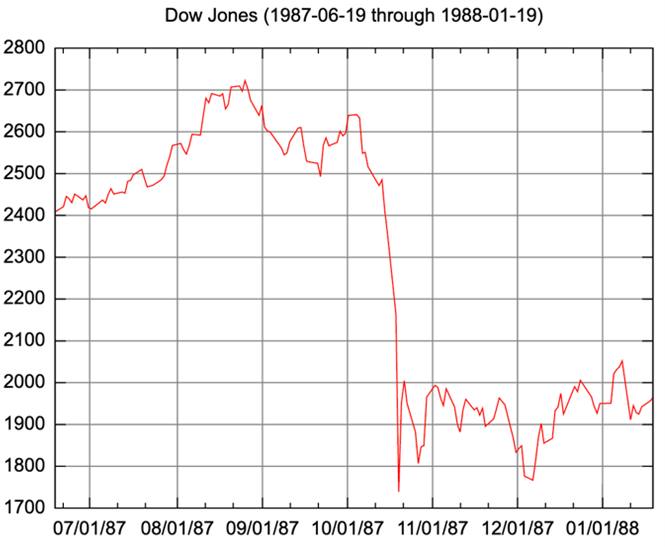

Bull Markets Take the Stairs…Bear Markets Take the Elevator Shaft

When this flight to safety occurs en masse, the mutual funds and ETF’s have to sell many of the most popular stocks in their portfolio to raise cash. Heavy selling activity drives stock prices down. Negative price action can trigger margin calls and more forced selling. You may have thought your portfolio was asset class differentiated only to find out that despite your thoughtful effort to balance your asset allocation, your funds hold many of the same stocks. Google Black Monday and you’ll see what I’m talking about.

On October 19, 1987, the Dow Jones Industrial Average fell 508 points (22.6%) making it the highest one-day drop in the index’s history. The Federal Reserve intervened to ensure bank liquidity and demands for credit were met. The DJIA began to recover in November of 1987. This calamitous, market-cap-crushing crash led the NYSE to develop and institute trading curbs and circuit breakers the following year to halt markets during a precipitous sell-off.

Diversify with Non-Correlated Returns

Senior Life Settlements are an answer to balancing volatility risk in your portfolio with non-correlated absolute returns. A diversified range of life insurance policies produces non-volatile yield because there’s no relationship between a life contract and anything else other than the mortality of the insured.

Over the course of time, maturity proceeds from policy death benefits flow through to subscribers as they occur. With a reinvestment of maturity proceeds into new portfolio positions to increase contract count, life settlements can produce a differentiated stream of non-correlated income well into the future.